Should I rent or buy business property? (video)

In this guide:

- Renting commercial property

- Should I rent or buy business property? (video)

- Advantages of renting commercial property

- Find commercial property to rent

- Commercial property rental agreements

- Renting commercial property: practicalities

- Costs when renting commercial property

- Alterations to rental properties

Should I rent or buy business property? (video)

Short video will help you decide whether renting or buying premises is best for your business needs.

This short video (5 minutes, 48 seconds) will help you identify whether you should rent or buy business property.

Also on this siteContent category

Source URL

/content/should-i-rent-or-buy-business-property-video

Links

Advantages of renting commercial property

The business benefits of renting property can range from better cashflow to having more flexibility if you need to relocate your business in the future.

Buying business property is a big commitment and it's important to consider carefully whether renting property may be a better option for your business.

Flexibility of renting business property

Renting business premises can provide more flexibility for your business as it grows. You are not locked into property ownership and you can usually agree with your landlord on the length of the rental lease that you require, or have a break clause included in the lease. This will let you end the rental lease (usually on a specific date) if, for instance, you want to relocate. See business tenant's rights to end a tenancy.

Renting a business property can also give you space for negotiation with the landlord. You or your agent can negotiate any aspect of the rental lease, either at the start or if you want to renew it after the rental lease ends.

Financial benefits of renting business property

From a financial perspective, renting property can make good business sense. Upfront costs for leasing premises are often relatively low, though you may pay a premium to purchase the lease. Sometimes you may also have to provide a refundable deposit. But generally renting ties up less capital than buying business property, freeing up cash that could be used elsewhere in the business. See renting business property: practicalities.

If you rent your business property you are not exposed to interest rate rises, although your rent may rise periodically as a result of rent reviews. Always check to see how rent is reviewed before you sign the rental lease. See business leases: paying rent and rent reviews.

There is also less potential for unexpected economic fluctuations such as a decrease in property value - unless you wish to sell the remaining term on your rental lease to someone else. Also, you will not have to pay Capital Gains Tax unless you decide to sell your rental lease for a premium.

Maintenance responsibility in rented business property

You may have less responsibility for the building if you rent rather than buy a business property, although this will depend on the terms of your rental lease. As a tenant you may have responsibility for repairs and maintenance inside the building but external maintenance is more likely to be the responsibility of the landlord, particularly in multi-occupancy premises. Be mindful that you may have to pay a service charge as part of your rental agreement. See commercial property: landlord and tenant responsibilities.

Also on this siteContent category

Source URL

/content/advantages-renting-commercial-property

Links

Find commercial property to rent

Your options to find suitable business premises to rent including how to use a commercial agent to search for you.

There are a number of ways to search for appropriate business property to rent.

How to find a business property to rent

To begin your search for business property to rent you could consider:

- using our commercial property finder tool

- visiting a local estate agent in person

- searching estate agent websites

- touring your local area to see agents' letting boards outside the business property for let

- property listings in local newspapers

- your local council - through their Economic Development Unit

- trade associations - if an existing member is retiring or selling up their business

Commercial agents

Another good way to find a suitable business property to rent is by appointing a commercial agent or commercial surveyor to search on your behalf. You can find a commercial surveyor near you.

Commercial agents and surveyors have expertise in the business property market in the area and can keep you up to date with any new commercial property that comes onto the market for rent. They will also send you detailed specifications of a suitable property, which can be very useful, particularly if you are limited by time.

You must pay a commission to a commercial agent for acting as an intermediary between you and the landlord or seller. You will need to fully brief the agent, manage the relationship well and maintain regular contact to ensure that they find you the most suitable property.

When employing an agent to act on your behalf, you should also draw up a contract, even if the relationship is informal. This will help to set out expectations and clarify your legal obligations to them from the start. See sell through a commercial agent.

Also on this siteContent category

Source URL

/content/find-commercial-property-rent

Links

Commercial property rental agreements

An overview of the types of property rental agreements available to businesses looking to rent premises.

You can rent business property by leasing it. If you require premises for a short term, for example, to complete an unusually large order, then consider a licence rather than a lease.

Leasing business premises

Leases typically have agreements of between three and 25 years and can offer long-term stability for your business.

You will probably be able to negotiate the length of your rental lease with your landlord and should certainly check before signing the contract. You should also seek legal advice - see choose a solicitor for your business.

Other than the rent itself, key areas of the contract that you should study include:

- lease length

- break clauses

- service charges

- dilapidations (an amount payable to the landlord at the end of the lease)

- responsibility for maintenance and repairs to the building and external areas

Lease length

Rent is usually paid quarterly in advance. However, you may be able to pay monthly. This can form part of negotiations with your landlord. If your business is new, you may want to consider a short lease of three years or less. You may also want to ask for a break clause.

Service charges in rental properties

Check how much service charges are and which services they specifically cover, such as cleaning and heating. Establish what facilities you may be sharing with other tenants. Service charges are an additional cost to the rent and can be more expensive than if you organise them yourself.

You have the right to ask the landlord for a summary of how the service charge is calculated and for any paperwork supporting the summary eg receipts. Your landlord must provide this information as it is a criminal offence not to. See service charges in commercial property.

You have the right to remain in occupation of the premises and renew the lease once it expires unless you and your landlord have agreed otherwise. However, there are specific cases when the landlord can refuse to grant a renewal. See business leases: renewing and ending.

Licensing business premises

A licence could be of benefit to a small business looking for a short-term property rental solution, of up to one year. Licences generally offer more flexibility and can usually be terminated at short notice on both sides. However, you would not have an automatic right to renew a licence and it is always advisable to seek professional advice, eg from a chartered surveyor or solicitor before pursuing it.

Also on this siteContent category

Source URL

/content/commercial-property-rental-agreements

Links

Renting commercial property: practicalities

The costs, considerations and obligations of renting business property.

There are a number of practical issues to consider when you rent a business property.

Rental property contracts

Contracts when renting business premises can be complex, so consider professional help from a solicitor or chartered surveyor. While this can be expensive, mistakes can be much more costly to remedy.

You can find a surveyor in your area or find details of local solicitors.

Planning permission for rental properties

Before renting business premises, make sure you have planning permission to make any changes you need to the property. See alterations to rental properties. You should also investigate whether the building has asbestos.

Find out if there are any restrictions on delivery or loading times that may affect your business. There may be other restrictions or covenants in the lease or imposed by the local council - for example, rubbish disposal, parking, noise, lighting, and litter. Find your local council in Northern Ireland.

Land registration

The Department of Finance provides guidance on how to register land in Northern Ireland, and the associated fees.

Insurance for rental properties

The business lease will state whether you or the landlord need to arrange insurance for the property. If the landlord arranges this, you will pay the premiums as part of the service charges. Therefore, you may need to take out additional insurance to cover risks, such as loss or damage to contents, which are not covered in the building policy. See insurance: business property and assets.

Also on this siteContent category

Source URL

/content/renting-commercial-property-practicalities

Links

Costs when renting commercial property

Financial commitments when renting business premises, including rent, bills and taxes.

Your financial commitments when renting business property can include:

- a premium to purchase the lease

- rental costs

- service charges

- utility bills

- maintenance and repair bills

- a deposit - typically equivalent to three or six months' rent

- stamp duty, which is payable on all commercial leases

- business rates - estimate your rate bill

Normally, the landlord will request references to confirm you are able to pay your rent and meet your rates liability. You may find it helpful to have a guarantor for your rent and other liabilities under the lease.

Energy costs for rental properties

All landlords of commercial buildings must provide prospective tenants with an Energy Performance Certificate (EPC). An EPC indicates how energy efficient a building and its services are and can act as a gauge of likely energy costs. See Energy Performance Certificates for business properties.

Air conditioning and heating systems can have a significant effect on your overall energy bills. You can make substantial savings by keeping these well-maintained and having them inspected often by a qualified engineer. See use heating and hot water systems efficiently.

ActionsAlso on this siteContent category

Source URL

/content/costs-when-renting-commercial-property

Links

Alterations to rental properties

Issues to consider before you alter your rented business premises, such as planning permission, asbestos, and liability.

There are a number of issues to consider before you alter the business premises that you are renting.

Planning permission

Planning permission is not always required if you wish to make alterations to the property, for example, if you want to make changes to the inside of the building or minor alterations to the outside. Also, a specific application is not needed if you want to put up low walls or fences, although you should always check whether building regulations are required by contacting the building control section at your local council.

However, planning permission is generally required if you want to extend, convert or change the external nature of the premises. It is always a good idea to check with your local planning authority whether the development will require planning permission at the proposal stage. The majority of significant building work also has to conform to building regulations. Planning permission.

Landlord's permission

Before you start any alteration work, you should check the details of the rental lease. You may need to get permission from the landlord. Unless the lease expressly prohibits improvements, the landlord may not unreasonably withhold consent to tenants' improvements. Also, you should clarify whether you will be required to reinstate the property to its original condition before the agreement expires.

Energy Performance Certificate

If you change the number of units that the property is divided into (for example dividing one shop unit into two or merging two into one), which include fixed services for heating, hot water, air conditioning, or mechanical ventilation, an Energy Performance Certificate will be required when the work is completed. It is the responsibility of the person carrying out the building work to provide the certificate.

Asbestos

Before any alterations are made you should consider whether asbestos might be present within the property.

Rateable value

You should also check whether the works you are planning will alter your rateable value. The rateable value of business premises is based on their open market rental value. Changing your premises may affect this. See property changes and business rates.

Repairs to rental properties

You also need to be aware of the liability for repairs. If you rent workspace in multi-occupancy premises, liability for external repairs and maintaining common areas is likely to fall with the landlord. Check the terms of the lease to find out who is responsible.

You should also check the rental agreement to see whether there is any repair work pending. You may decide to commission a survey and ensure that any such work is finished before the rental agreement is signed in order to avoid paying the bill.

Also on this siteContent category

Source URL

/content/alterations-rental-properties

Links

Deciding on the right premises for your business (video)

In this guide:

- Choosing the right commercial property

- Business property specification

- Choose the right location for your business premises

- Legal considerations when choosing business property

- Deciding on the right premises for your business (video)

- Search for commercial property

- Six tips for choosing the right business property

- Choosing the right premises to suit our business needs - Totalmobile (video)

Business property specification

How to draw up a wish list that sets out what you want when searching for suitable commercial premises.

Preparing a clear business property specification is an important first step when choosing commercial property. A well-defined property spec helps you focus your search for commercial premises, compare options consistently, and avoid wasting time on unsuitable business property.

What is a property specification?

A business property specification, or property spec, is a written list of what you need from your commercial premises for business. It sets out your essential and desirable requirements. It guides your search for business premises to rent or buy, whether you are looking at larger sites or commercial properties for a small business.

Key points to include in your property spec

Your property spec might detail how the following requirements should be met when looking for suitable commercial real estate or business premises.

Property size and layout

Decide how much space you need now and, in the future, based on staff numbers, equipment and storage. Consider whether an open-plan layout, individual offices, or a mix of both will work best, and whether you need extra areas for equipment, storage, meetings, breakout spaces or socialising.

Property appearance

Think about how the business property looks both inside and out. If clients or customers will visit regularly, you may need a more visually attractive exterior and a professional, welcoming interior that reflects your brand and creates a good first impression.

Property structure

Identify any special structural requirements. For example, you may need high ceilings, upper-floor loading capacity, reinforced floors or foundations, or specific loading doors or access arrangements to support your operations.

Premises facilities

Consider the comfort and wellbeing of employees and visitors. Make a note of the standard of lighting, toilet and washrooms, reception or waiting areas, kitchen or tea points, and any staff welfare or breakout facilities you require.

Property utilities and connectivity

List the utilities and services you need for your commercial property to operate efficiently. This can include:

- adequate power supply and type (for example, three-phase electricity)

- heating and cooling systems to maintain comfortable working conditions

- sufficient power points for computers and equipment

- suitable water supply and drainage

- broadband speed and reliability, including fibre availability

Older buildings may need rewiring, upgraded heating or air conditioning, or additional toilet and kitchen facilities, so factor potential upgrade costs into your planning.

Planning permission and use

Check whether you may need planning permission or a change of use to run your type of business from the premises. Understanding this early can help you avoid delays or unexpected costs once you have chosen your commercial premises.

Access and parking

Think about how people and goods will reach your business property. Consider:

- proximity to main roads and public transport

- ease of access for deliveries and collections

- accessibility for customers, including disabled customers

- on-site or nearby car parking for staff, customers and visitors

- any need for cycle parking or other sustainable transport options

Option to extend or make alterations

Assess how flexible the commercial real estate is if your requirements change. Look at whether you can make internal alterations, install partitions, expand into neighbouring space, or extend the building in future, subject to any necessary consents.

Long-term business plans

Review your business plan and consider how the business premises you choose will support your long-term direction. Think about potential growth, new services or products, changes in staffing levels, or future technology needs, and whether the property can adapt to these.

Property location

Location is a crucial factor when choosing commercial property. You need to think about where your property should be to suit your customers, workforce and suppliers, as well as your brand image and operational needs. For detailed location factors you should consider, see choose the right location for your business premises. See, choose the right location for your business premises.

Property costs

Your choice of commercial property will also depend on your budget. Whether you rent or buy business premises, likely costs can include:

- initial purchase costs (if buying property), including legal costs and surveyor's fees

- initial alterations, fitting out and decoration

- any alterations required to meet building, health, safety and fire regulations

- ongoing rent (if leasing premises), service and utility charges, including water, electricity and gas

- business rates

- continuing maintenance and repairs

- building and contents insurance

It can be useful to compare the costs of buying business property with the costs of buying business property so you can decide which option is more suitable for your cash flow and growth plans.

Energy performance of the property

Energy efficiency affects both your running costs and environmental impact. Sellers and landlords must provide prospective buyers or tenants with an Energy Performance Certificate (EPC). An EPC shows how energy efficient a building and its services are and provides a good indication of likely energy costs. You may wish to prioritise commercial property for small businesses that offer better energy performance to help control long-term overheads. See Energy Performance Certificates for business properties.

Prioritising your requirements

If your property requirements are too specific, your choice of commercial premises for business may become very limited or too expensive. Divide your property spec into:

- essential requirements that you cannot compromise on

- desirable features that are beneficial but negotiable

This helps you stay flexible and make a balanced decision when comparing different commercial property options.

Considering working from home

Once you have drawn up your list of property requirements, you may decide that working from home suits your needs better, either full-time or as part of a hybrid model. If so, remember that there are important legal, tax and practical issues to consider, including planning, insurance and health and safety. See use your home as a workplace.

Also on this siteMore Case StudiesContent category

Source URL

/content/business-property-specification

Links

Choose the right location for your business premises

How to identify the advantages and disadvantages when choosing a suitable location for your commercial property.

Choosing the right location for your commercial property is a vital decision for any business. Your business premises should be convenient for customers, employees and suppliers, while still being affordable and aligned with your long term plans. When choosing commercial property, you should weigh up the advantages and disadvantages of different locations before committing to any business property.

What location factors should I consider when looking for business property?

To judge the best location for your commercial premises for business, consider the key factors below and how important each one is to your business priorities. These points apply whether you are looking for business premises to rent, business premises to buy, or specific commercial property for a small business.

Footfall

For many businesses – especially in the retail, hospitality or personal services sectors – the level of passing trade can have a major impact on sales and visibility. Busy high streets, shopping centres, or transport hubs can provide higher footfall but usually come with higher commercial real estate costs and business rates.

Competitors in the area

The number and type of competitors nearby can significantly affect your performance. Some businesses, such as estate agents or restaurants, can benefit from clustering together, as customers often compare options in one area. For many other firms, too many direct competitors close by can reduce your market share and profitability, so it is worth surveying the local area carefully before choosing your business property.

Transport links and parking

Good public transport links and local parking facilities make it easier for employees, customers and suppliers to reach your commercial property. Check proximity to bus routes, train stations, cycle paths and major roads, and consider whether there is sufficient, affordable parking nearby for staff and visitors.

Delivery restrictions

If your business relies on regular deliveries or collections, it is important that your commercial premises for business are easy for vehicles to access. Investigate any delivery time restrictions, loading bay rules, or weight limits that could affect your suppliers or logistics operations.

Planning restrictions

Before you commit to a location, make sure the premises can legally be used for your type of business. Check planning permission and local zoning or use classes to ensure your activity is permitted, and identify any restrictions that might limit how you operate or expand in future.

Business rates

Business rates can be a major ongoing cost and vary depending on property value and location. High-profile city or town centre locations can attract higher rates, which may reduce the attractiveness of otherwise ideal business premises to rent or buy. It is important to get an indication of what you may have to pay so you can factor it into your overall budget. See estimate your rate bill.

Local amenities

Local amenities can make a location more attractive for both employees and customers. Staff often prefer working in areas with nearby shops, cafés, childcare, gyms and other services. You may also need convenient access to banking facilities, postal depots and professional services to support day-to-day operations in your commercial property.

Type and image of an area

The nature and reputation of the area can affect how your business is perceived. A location associated with high crime or anti-social behaviour may deter customers and staff, while a well-regarded business district or regeneration area can enhance your image. Think about how the area aligns with your brand and the clients you want to attract when choosing commercial property.

Deciding on your property location

Every location will have both advantages and disadvantages, so finding the right business property is often a balancing act. For example, an office in a rural setting may be quieter and cheaper, but harder for staff, customers or suppliers to access. A prime city centre site may be excellent for visibility and transport links, but more expensive in terms of property costs, business rates and parking.

Location has a major impact on your overall business costs and on the value you get from your commercial real estate. If you need premises in a prime area – for example, to access key clients or benefit from strong footfall – the extra cost may be justified. The key is to prioritise the factors that matter most to your strategy and choose commercial property that offers the best overall fit for your business.

Also on this siteMore Case StudiesContent category

Source URL

/content/choose-right-location-your-business-premises

Links

Legal considerations when choosing business property

What legal obligations and restrictions to consider when choosing commercial premises.

When choosing commercial property, it is essential to understand the legal obligations and restrictions that apply to your business property. These rules affect both owners and occupiers and will influence the suitability of any commercial premises for business, whether you are looking for business premises to rent or business premises to buy.

Planning permission and permitted use

Your commercial property must have the correct planning permission or use class for your type of business. If you intend to change how the property is used, extend it, or alter its layout, you may need to apply for new planning consent or building control approval.

Failing to comply with planning requirements can lead to enforcement action, so always check permitted use before committing to any commercial property for a small business or larger operation.

Building, fire and health and safety compliance

All commercial property must meet relevant building regulations and fire safety standards. You will need to carry out suitable fire risk assessments, maintain fire detection and alarm systems where required, and ensure that escape routes, emergency lighting and fire-fighting equipment are appropriate for your business premises.

You must also comply with health and safety law to protect employees, contractors and visitors, including providing safe access, adequate ventilation, lighting, welfare facilities and a generally safe working environment. See fire safety and risk assessment.

Business rates, stamp duty and other charges

Most business premises to rent or buy will attract business rates, based on the property’s rateable value and local rules. In many cases, stamp duty land tax (or the relevant property tax) is payable on commercial property purchases and some leases, so factor this into your budget alongside rent or mortgage payments.

Clarify in advance whether the landlord or tenant is responsible for business rates, service charges and other recurring costs before you sign any agreement for commercial premises for business.

Landlord, tenant and lease obligations

If you occupy business premises to rent, the terms of your lease or licence will set out your rights and responsibilities. These may cover rent reviews, repairing obligations, service charges, use restrictions, alterations, subletting, break clauses and how and when the lease can be ended.

You should ensure that any lease for commercial real estate is clearly understood and, where possible, professionally reviewed so you know exactly what you are committing to over the term. See commercial property: landlord and tenant responsibilities.

Employer duties and workplace conditions

If you employ staff in your commercial property, you are responsible for their health, safety and welfare while at work. This includes providing suitable welfare facilities (such as toilets, washing facilities, drinking water and rest areas), a healthy indoor environment and safe systems of work.

You must identify and manage workplace risks, maintain equipment safely and ensure your business property is suitable for the number of people working there. See workplace welfare facilities and healthy working environment.

Accessibility and equality requirements

If you provide goods or services to the public, you must take reasonable steps to make your commercial premises for business accessible to disabled people. This may involve ramps or step-free access, appropriate signage, accessible toilets, suitable door widths or layout changes.

Considering accessibility early, when choosing commercial property, can save costs and reduce the risk of failing to meet equality and anti-discrimination duties. See disabled access and facilities in business premises.

Operating licences, restrictions and environmental controls

Certain types of business activity require licences or permits – for example, selling alcohol, handling specific waste types or operating some regulated services. There may also be conditions on when deliveries can take place, limits on noise levels, restrictions on emissions, and rules on waste storage and disposal. Before you choose business premises to buy or rent, check whether your activities will need additional permissions or be affected by local environmental or neighbourhood restrictions.

Insurance for business property and assets

Whatever commercial property you occupy, adequate insurance is essential. Common policies include buildings insurance (if you are responsible for the structure), contents and equipment insurance, public liability, employer’s liability and business interruption cover.

Check what the landlord insures, what you must insure yourself, and whether your chosen commercial property for a small business presents any special risks that need extra cover. See insurance: business property and assets.

Getting professional legal advice

Legal requirements around commercial real estate can be complex and may vary depending on location, sector and property type. Before signing a lease, purchase contract or licence, it is sensible to seek advice from a suitably qualified solicitor or business adviser experienced in commercial property. They can help you interpret legal documents, identify hidden risks and ensure the business property you choose is compliant and suitable for your plans. Choose a solicitor for your business.

More Case StudiesContent category

Source URL

/content/legal-considerations-when-choosing-business-property

Links

Deciding on the right premises for your business (video)

Short video outlines key factors to consider when deciding on suitable business premises.

View this short video (2 minutes 30 seconds) below that outlines important factors to consider when deciding on the right business premises. It explores issues such as cost, location, facilities, and infrastructure.

Also on this siteContent category

Source URL

/content/deciding-right-premises-your-business-video

Links

Search for commercial property

Specifying what you want when searching for business premises and where you can search for suitable commercial property.

Starting your search for commercial property by drawing up a clear business property specification is one of the most effective ways to find suitable commercial premises for business. A well-defined “property spec” sets out your essential and desirable requirements, helps you prioritise location and property features, and makes it easier to compare different business premises to rent or business premises to buy.

Define what you need before you search for a property

Begin by creating a written specification that clearly describes what you need from your business property. Include details such as size, layout, facilities, utilities, accessibility, budget range, and preferred locations, and highlight which points are non-negotiable and which are flexible. This will guide your decisions when choosing commercial property and reduce the time spent viewing unsuitable options.

Where to search for commercial property

There are several ways to search for commercial property for small businesses and larger organisations in Northern Ireland and across the UK:

- Use dedicated tools such as our commercial property finder, which provides access to a wide range of office, industrial, and other commercial listings across Northern Ireland.

- Search specialist commercial and mixed-use listings on local portals such as PropertyPal and national platforms like Rightmove and other major commercial property websites.

- Visit individual estate agents’ and commercial surveyors’ websites, where many agents advertise local commercial property to rent or for sale.

As you find options, check each potential property against your specification and remove any that do not meet all of your essential criteria. You can then create a shortlist of business properties to visit in person, focusing only on those that match your priority needs.

Professional advice during your property search

At the viewing and negotiation stage, it is often helpful to seek professional advice. A qualified surveyor can assess the condition of a property, highlight any structural or maintenance issues, and give you an informed view on value and suitability for your intended use. See buying commercial property: using a surveyor.

When you are ready to make an offer or agree on lease terms, a solicitor experienced in commercial real estate can help negotiate the deal and handle the legal work involved in renting or buying business premises. See buying commercial property: using a solicitor.

Taking these steps will help you conduct a focused, efficient search for commercial premises, making it easier to secure the right property in the right location for your business.

Also on this siteMore Case StudiesContent category

Source URL

/content/search-commercial-property

Links

Six tips for choosing the right business property

Six tips to help you find a suitable commercial property to buy or rent for your business.

Choosing commercial property is easier when you follow a clear, step-by-step process that keeps your business needs, budget, and long-term plans in focus. These six tips will help you narrow down suitable commercial premises for business, whether you are looking for business premises to rent or business premises to buy.

Top tips to help you find suitable commercial premises

1. Draw up a clear business property specification

Start by listing what you need from your business property before you begin viewing sites. Consider property size, layout, location, facilities, structural requirements, utilities, access, and parking, as well as your long-term business plans. Prioritise your requirements from must-haves to nice-to-haves so you can quickly rule out commercial properties that do not meet your essential needs.

See business property specification.

2. Don't underestimate the importance of location

Location can make or break the success of your commercial real estate. When choosing commercial property, think about customer footfall, where your competitors are based, local demographics, delivery and parking restrictions, transport links, and overall safety and image of the area. The right location for your commercial property for a small business might be a busy high street, a growing business park, or a well connected out of town site, depending on how your customers find and use your services.

See choosing the right location for your business premises.

3. Decide whether to buy or rent a commercial property

You will need to determine if buying or renting commercial property is best for your stage of growth and cash flow. Compare the flexibility of business premises to rent (typically lower upfront costs and easier to move) with the control and potential long term value of business premises to buy. Consider how long you expect to stay, how quickly your space needs might change, and whether tying up capital in commercial real estate is right for your overall business strategy.

See the advantages of renting commercial property versus the advantages and disadvantages of buying business property.

4. Calculate business rates and ongoing property costs

Before agreeing to rent or buy, estimate what you are likely to pay in business rates and other recurring charges for a particular commercial property. Factor in rent or loan repayments, service charges, utilities, insurance, maintenance, repairs, and any local taxes so you have a realistic total occupancy cost. Check whether you may qualify for any business rates reliefs or local support schemes that could make a specific commercial premises for business more affordable.

See help available for business rates.

5. Check the legal considerations for commercial property

Every business property is subject to legal requirements, so build these into your decision. Make sure the premises have the correct planning permission or use class, and that you can comply with building regulations, health and safety, fire safety, accessibility rules and any licensing requirements. If you are renting, review lease terms carefully – including break clauses, repairing obligations and use restrictions – and take advice from a solicitor experienced in commercial real estate before you sign.

See legal considerations when choosing business property.

6. Search widely and compare options for commercial property

Use multiple channels to search for commercial property, including local commercial agents, specialist online portals and regional property finders. Check each potential property against your specification, discard any that fail to meet your essential criteria, and then draw up a shortlist of business properties to view in person. Visiting several suitable sites will help you compare location, condition and value, and choose the commercial property that offers the best overall fit for your business needs.

Also on this siteMore Case StudiesContent category

Source URL

/content/six-tips-choosing-right-business-property

Links

Choosing the right commercial property

Choosing the right premises to suit our business needs - Totalmobile (video)

Video case study explaining how Totalmobile found the right premises to suit the needs of their growing business.

Malcolm Thompson, Chief Operating Officer of software provider Totalmobile, explains how they chose new premises to suit the needs of their growing business.

As Totalmobile expanded and its requirements changed, the business decided to move from its premises in the Antrim Technology Park to new rented premises in Belfast. The business had to consider various factors in order to make the right choice.

Here, Malcolm and Chief Executive Colin Reid discuss how the business identified the right premises and overcame the challenges of the move.

Case StudyMalcolm ThompsonContent category

Source URL

/content/choosing-right-premises-suit-our-business-needs-totalmobile-video

Links

Rates for licensed premises

Business rates and types of premises

Types of property that must pay business rates and those that are excluded.

Business or non-domestic premises include most commercial properties, such as shops, offices, pubs, warehouses, and factories.

Properties excluded from the valuation list for business rates

There are some types of properties that are specifically excluded from the valuation list and therefore not subject to rates:

- fish farms

- most farmland and farm buildings

- most cemeteries and crematoriums

- turbary and fishing rights

- moveable moorings

- public parks

- sewers

Properties exempt or partially exempt from business rates

Some non-domestic premises that are exempt or partially exempt from rates include:

- places of public religious worship and church halls

- district council swimming pools and recreation facilities

- charity shops selling only donated goods

- ATMs in designated rural wards

Mixed-use properties and business rates

If part of a building is used for business and part for residential purposes - such as a shop with a flat above or a solicitor's office in a domestic property - the part used for business counts as non-domestic premises. So, if you live and work on the same premises, you generally pay business rates on the part of the property used for business and domestic rates on the residential part.

Rental properties and business rates

Special rules apply to landlords, owners, and tenants depending on the level of Capital Value for domestic properties or Net Annual Value for non-domestic properties. Rental properties and business rates.

Working from home and business rates

If you use your home as a workplace, the part of the property used for work may be liable for business rates. You will still have to pay domestic rates on the rest of the property. Whether you are charged business rates or not depends on the degree of business use. You are more likely to have to pay business rates if a room is used exclusively for business or has been modified, eg, as a workshop. Each case is considered individually.

Further information

If you have a query regarding your business rates, contact Land & Property Services.

Developed withAlso on this siteContent category

Source URL

/content/business-rates-and-types-premises

Links

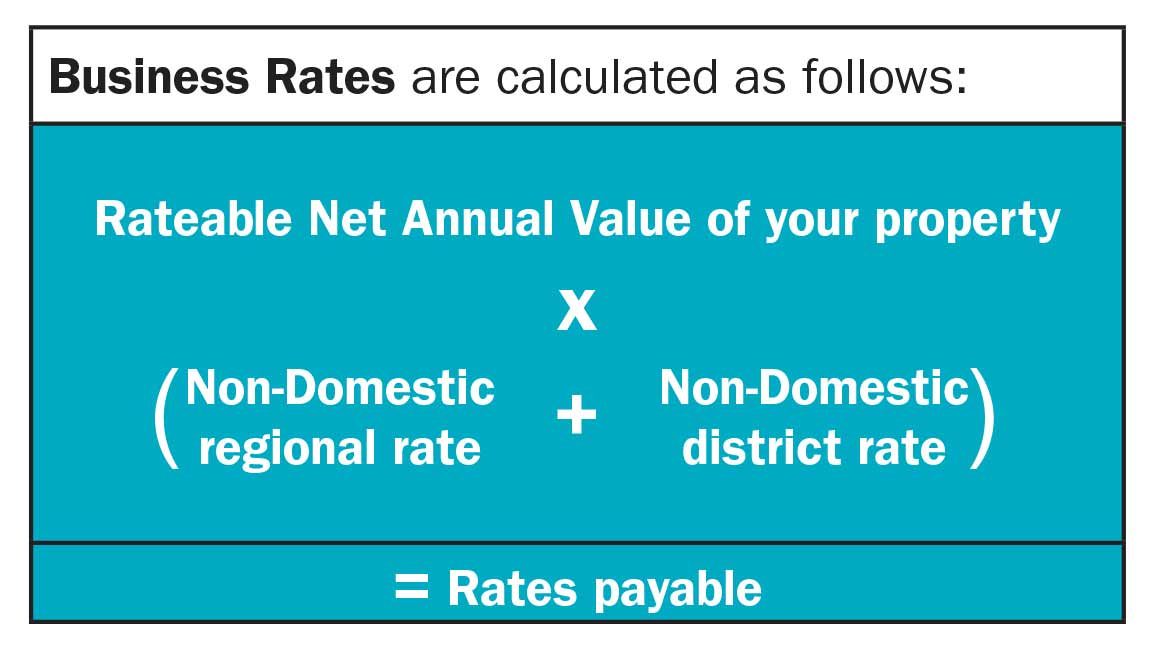

How business rates are calculated

How rates are calculated for business premises and how to get an idea of what your rate bill may be.

Your rate bill is made up of a number of parts including the regional rate, the district rate and Net Annual Value (NAV). Your rate bill is calculated by multiplying the NAV of your property by the non-domestic rate poundage (non-domestic regional rate + non-domestic district rate) for your council area for the relevant year (as shown below):

Regional and district rates

The regional rate is set annually by the Northern Ireland Executive and is applied to each district council area in Northern Ireland. The district rate is set annually by each district council in Northern Ireland.

Find the the 2026-27 non-domestic rate poundages for your council area.

Net Annual Value

Rates for non-domestic or business properties are assessed on their rental value, also known as the Net Annual Value (NAV). NAV is an assessment of the annual rental value that your property could reasonably be expected to be let for if it was on the open market. Each non-domestic property is valued in line with comparable properties in the vicinity.

The current valuation list for non-domestic properties began on 1 April 2023 and is based on rental values as at 1 October 2021.

Find a property valuation for your business premises.

View your estimated rate bill

You can view an estimate of a full annual rate bill for the current rating year by inputting the address information using the Land & Property Services (LPS) online valuation search.

Find a property valuation and view your estimated rate bill.

Further information

If you have a query regarding business rates or are unsure of your outstanding bill, contact LPS.

NI Reval2026

The short video below explains the latest revaluation process, known as NI Reval2026, which will create a new valuation list that will be used to calculate business rate bills from April 2026.

Developed withAlso on this siteContent category

Source URL

/content/how-business-rates-are-calculated

Links

Rates for retail units

How business rates are calculated for retail units and how this differs from other types of non-domestic properties.

When calculating business rates for retail units Land & Property Services (LPS) assess the Net Annual Value (NAV) by using zoning. Zoning is a methodology used in assessing the rental value of retail units and is used for shops, hair salons, banks, betting shops and most restaurants. LPS use zoning as it helps take into account different sizes and shapes of shops and awkward layouts.

LPS also consider other parts of the property that are ancillary or tertiary spaces such as upstairs offices and store rooms. They are rated but zoning is not applied for these areas of the property. Some spaces are not considered useable retail areas and are excluded from valuation. These spaces include toilets, lobbies, plant rooms and stairwells.

Further information

If you have a query regarding business rates, contact LPS.

NI Reval2026

On Thursday 29 January 2026, the Finance Minister John O'Dowd announced a pause of the Reval 2026 process. This page will be updated when the next steps are confirmed.

The short video below explains the latest revaluation process, known as NI Reval2026, which will create a new valuation list that will be used to calculate business rate bills from April 2026.

Developed withAlso on this siteContent category

Source URL

/content/rates-retail-units

Links

Rates for licensed premises

How business rates are calculated for licensed premises and how this differs from other types of non-domestic properties.

When calculating business rates for licensed premises, Land & Property Services (LPS) assess the Net Annual Value (NAV) by calculating the correct level of Fair Maintainable Trade (FMT). LPS does this by collecting information about rent, trading receipts, and trading patterns. LPS analyses this information along with the type of premises, the area it is in, and what services it offers.

As there is little evidence of rents for pubs, LPS uses FMT in the assessment to help assess a rateable value or NAV. This is the industry standard and is the approach used across the UK.

LPS applies a percentage to the estimated FMT to assess the annual rent. It is based on factors such as, where the premises are located, the sort of premises they are (bar, hotel, etc.), and the sort of trade carried on. LPS regularly consults with trade associations to ensure its approach continues to reflect how the licensed industry operates.

Further information

If you have a query regarding business rates, contact LPS.

NI Reval2026

On Thursday 29 January 2026, the Finance Minister John O'Dowd announced a pause of the Reval 2026 process. This page will be updated when the next steps are confirmed.

The short video below explains the latest revaluation process, known as NI Reval2026, which will create a new valuation list that will be used to calculate business rate bills from April 2026.

Developed withAlso on this siteContent category

Source URL

/content/rates-licensed-premises

Links

Business rates: Occupying, leaving or vacating a property

How your business rates are affected if you occupy, leave, or vacate a property and how to inform Land and Property Services of changes.

Moving into a new business property

When you move into your new property, you must contact Land & Property Services (LPS) Rating office to let them know, otherwise you may receive a backdated rate bill. You can also advise them of how you wish to pay your rate bill.

Moving into a newly built business property

If you are moving into newly built premises, you must contact the LPS Valuation office. A valuer will come out to assess your property. A rate bill will then be issued based on this valuation. You should be aware that failure to inform LPS could lead to the issue of a backdated rate bill.

You can apply online to have your new property valuation assessed, or you can apply for a new property valuation or review of property valuation.

This is a writable document, which means that you can complete it on screen and send it as an attachment by email to print and send to the LPS Valuation office. You can also print and post it to LPS using the address on the form.

Leaving your old business property

When you move out of your property, you must contact LPS. You should have your Account ID, Ratepayer ID, and details of the new owners or people in your property to hand.

Alternatively, you can use the online form to make changes to your rate account, such as personal information, billing address for your rate bill, notification of a ratepayer's death, or change the assessment period for your rate account.

You can also make changes to your rate account through your Rates Online account.

Further information

If you have a query regarding business rates, contact LPS.

Developed withAlso on this siteContent category

Source URL

/content/business-rates-occupying-leaving-or-vacating-property

Links

How Land & Property Services uses your information

How LPS uses customer data and how they protect this data under the legislation.

Land & Property Services (LPS) fully complies with the Data Protection Act 2018 and the Department of Finance's Data Protection Policy. This means that how LPS collects, stores, uses, and discloses/shares the information you provide to them meets the standards of this legislation.

Reasons why LPS collates and holds customer information

LPS holds customer information for:

- the purpose of billing

- collection and recovery of rate revenue

- assessment of benefit/relief claims

- the creation and maintenance of Valuation Lists

- the Land Registration Public Register

LPS and the National Fraud Initiative

LPS has a duty to protect public funds and may use the information provided for the prevention and detection of fraud.

LPS participates in the National Fraud Initiative, an exercise that matches electronic data within and between audited bodies to prevent and detect fraud.

The use of data by the Audit Commission does not require the consent of the individuals concerned under the Data Protection Act 2018. However, it is controlled to ensure compliance with data protection and human rights legislation.

For more information, contact LPS.

Developed withAlso on this siteContent category

Source URL

/content/how-land-property-services-uses-your-information

Links

Rates for retail units

Business rates and types of premises

Types of property that must pay business rates and those that are excluded.

Business or non-domestic premises include most commercial properties, such as shops, offices, pubs, warehouses, and factories.

Properties excluded from the valuation list for business rates

There are some types of properties that are specifically excluded from the valuation list and therefore not subject to rates:

- fish farms

- most farmland and farm buildings

- most cemeteries and crematoriums

- turbary and fishing rights

- moveable moorings

- public parks

- sewers

Properties exempt or partially exempt from business rates

Some non-domestic premises that are exempt or partially exempt from rates include:

- places of public religious worship and church halls

- district council swimming pools and recreation facilities

- charity shops selling only donated goods

- ATMs in designated rural wards

Mixed-use properties and business rates

If part of a building is used for business and part for residential purposes - such as a shop with a flat above or a solicitor's office in a domestic property - the part used for business counts as non-domestic premises. So, if you live and work on the same premises, you generally pay business rates on the part of the property used for business and domestic rates on the residential part.

Rental properties and business rates

Special rules apply to landlords, owners, and tenants depending on the level of Capital Value for domestic properties or Net Annual Value for non-domestic properties. Rental properties and business rates.

Working from home and business rates

If you use your home as a workplace, the part of the property used for work may be liable for business rates. You will still have to pay domestic rates on the rest of the property. Whether you are charged business rates or not depends on the degree of business use. You are more likely to have to pay business rates if a room is used exclusively for business or has been modified, eg, as a workshop. Each case is considered individually.

Further information

If you have a query regarding your business rates, contact Land & Property Services.

Developed withAlso on this siteContent category

Source URL

/content/business-rates-and-types-premises

Links

How business rates are calculated

How rates are calculated for business premises and how to get an idea of what your rate bill may be.

Your rate bill is made up of a number of parts including the regional rate, the district rate and Net Annual Value (NAV). Your rate bill is calculated by multiplying the NAV of your property by the non-domestic rate poundage (non-domestic regional rate + non-domestic district rate) for your council area for the relevant year (as shown below):

Regional and district rates

The regional rate is set annually by the Northern Ireland Executive and is applied to each district council area in Northern Ireland. The district rate is set annually by each district council in Northern Ireland.

Find the the 2026-27 non-domestic rate poundages for your council area.

Net Annual Value

Rates for non-domestic or business properties are assessed on their rental value, also known as the Net Annual Value (NAV). NAV is an assessment of the annual rental value that your property could reasonably be expected to be let for if it was on the open market. Each non-domestic property is valued in line with comparable properties in the vicinity.

The current valuation list for non-domestic properties began on 1 April 2023 and is based on rental values as at 1 October 2021.

Find a property valuation for your business premises.

View your estimated rate bill

You can view an estimate of a full annual rate bill for the current rating year by inputting the address information using the Land & Property Services (LPS) online valuation search.

Find a property valuation and view your estimated rate bill.

Further information

If you have a query regarding business rates or are unsure of your outstanding bill, contact LPS.

NI Reval2026

The short video below explains the latest revaluation process, known as NI Reval2026, which will create a new valuation list that will be used to calculate business rate bills from April 2026.

Developed withAlso on this siteContent category

Source URL

/content/how-business-rates-are-calculated

Links

Rates for retail units

How business rates are calculated for retail units and how this differs from other types of non-domestic properties.

When calculating business rates for retail units Land & Property Services (LPS) assess the Net Annual Value (NAV) by using zoning. Zoning is a methodology used in assessing the rental value of retail units and is used for shops, hair salons, banks, betting shops and most restaurants. LPS use zoning as it helps take into account different sizes and shapes of shops and awkward layouts.

LPS also consider other parts of the property that are ancillary or tertiary spaces such as upstairs offices and store rooms. They are rated but zoning is not applied for these areas of the property. Some spaces are not considered useable retail areas and are excluded from valuation. These spaces include toilets, lobbies, plant rooms and stairwells.

Further information

If you have a query regarding business rates, contact LPS.

NI Reval2026

On Thursday 29 January 2026, the Finance Minister John O'Dowd announced a pause of the Reval 2026 process. This page will be updated when the next steps are confirmed.

The short video below explains the latest revaluation process, known as NI Reval2026, which will create a new valuation list that will be used to calculate business rate bills from April 2026.

Developed withAlso on this siteContent category

Source URL

/content/rates-retail-units

Links

Rates for licensed premises

How business rates are calculated for licensed premises and how this differs from other types of non-domestic properties.

When calculating business rates for licensed premises, Land & Property Services (LPS) assess the Net Annual Value (NAV) by calculating the correct level of Fair Maintainable Trade (FMT). LPS does this by collecting information about rent, trading receipts, and trading patterns. LPS analyses this information along with the type of premises, the area it is in, and what services it offers.

As there is little evidence of rents for pubs, LPS uses FMT in the assessment to help assess a rateable value or NAV. This is the industry standard and is the approach used across the UK.

LPS applies a percentage to the estimated FMT to assess the annual rent. It is based on factors such as, where the premises are located, the sort of premises they are (bar, hotel, etc.), and the sort of trade carried on. LPS regularly consults with trade associations to ensure its approach continues to reflect how the licensed industry operates.

Further information

If you have a query regarding business rates, contact LPS.

NI Reval2026

On Thursday 29 January 2026, the Finance Minister John O'Dowd announced a pause of the Reval 2026 process. This page will be updated when the next steps are confirmed.

The short video below explains the latest revaluation process, known as NI Reval2026, which will create a new valuation list that will be used to calculate business rate bills from April 2026.

Developed withAlso on this siteContent category

Source URL

/content/rates-licensed-premises

Links

Business rates: Occupying, leaving or vacating a property

How your business rates are affected if you occupy, leave, or vacate a property and how to inform Land and Property Services of changes.

Moving into a new business property

When you move into your new property, you must contact Land & Property Services (LPS) Rating office to let them know, otherwise you may receive a backdated rate bill. You can also advise them of how you wish to pay your rate bill.

Moving into a newly built business property

If you are moving into newly built premises, you must contact the LPS Valuation office. A valuer will come out to assess your property. A rate bill will then be issued based on this valuation. You should be aware that failure to inform LPS could lead to the issue of a backdated rate bill.

You can apply online to have your new property valuation assessed, or you can apply for a new property valuation or review of property valuation.

This is a writable document, which means that you can complete it on screen and send it as an attachment by email to print and send to the LPS Valuation office. You can also print and post it to LPS using the address on the form.

Leaving your old business property

When you move out of your property, you must contact LPS. You should have your Account ID, Ratepayer ID, and details of the new owners or people in your property to hand.

Alternatively, you can use the online form to make changes to your rate account, such as personal information, billing address for your rate bill, notification of a ratepayer's death, or change the assessment period for your rate account.

You can also make changes to your rate account through your Rates Online account.

Further information

If you have a query regarding business rates, contact LPS.

Developed withAlso on this siteContent category

Source URL

/content/business-rates-occupying-leaving-or-vacating-property

Links

How Land & Property Services uses your information

How LPS uses customer data and how they protect this data under the legislation.

Land & Property Services (LPS) fully complies with the Data Protection Act 2018 and the Department of Finance's Data Protection Policy. This means that how LPS collects, stores, uses, and discloses/shares the information you provide to them meets the standards of this legislation.

Reasons why LPS collates and holds customer information

LPS holds customer information for:

- the purpose of billing

- collection and recovery of rate revenue

- assessment of benefit/relief claims

- the creation and maintenance of Valuation Lists

- the Land Registration Public Register

LPS and the National Fraud Initiative

LPS has a duty to protect public funds and may use the information provided for the prevention and detection of fraud.

LPS participates in the National Fraud Initiative, an exercise that matches electronic data within and between audited bodies to prevent and detect fraud.

The use of data by the Audit Commission does not require the consent of the individuals concerned under the Data Protection Act 2018. However, it is controlled to ensure compliance with data protection and human rights legislation.

For more information, contact LPS.

Developed withAlso on this siteContent category

Source URL

/content/how-land-property-services-uses-your-information

Links

Six tips for choosing the right business property

In this guide:

- Choosing the right commercial property

- Business property specification

- Choose the right location for your business premises

- Legal considerations when choosing business property

- Deciding on the right premises for your business (video)

- Search for commercial property

- Six tips for choosing the right business property

- Choosing the right premises to suit our business needs - Totalmobile (video)

Business property specification

How to draw up a wish list that sets out what you want when searching for suitable commercial premises.

Preparing a clear business property specification is an important first step when choosing commercial property. A well-defined property spec helps you focus your search for commercial premises, compare options consistently, and avoid wasting time on unsuitable business property.

What is a property specification?

A business property specification, or property spec, is a written list of what you need from your commercial premises for business. It sets out your essential and desirable requirements. It guides your search for business premises to rent or buy, whether you are looking at larger sites or commercial properties for a small business.

Key points to include in your property spec

Your property spec might detail how the following requirements should be met when looking for suitable commercial real estate or business premises.

Property size and layout

Decide how much space you need now and, in the future, based on staff numbers, equipment and storage. Consider whether an open-plan layout, individual offices, or a mix of both will work best, and whether you need extra areas for equipment, storage, meetings, breakout spaces or socialising.

Property appearance

Think about how the business property looks both inside and out. If clients or customers will visit regularly, you may need a more visually attractive exterior and a professional, welcoming interior that reflects your brand and creates a good first impression.

Property structure

Identify any special structural requirements. For example, you may need high ceilings, upper-floor loading capacity, reinforced floors or foundations, or specific loading doors or access arrangements to support your operations.

Premises facilities

Consider the comfort and wellbeing of employees and visitors. Make a note of the standard of lighting, toilet and washrooms, reception or waiting areas, kitchen or tea points, and any staff welfare or breakout facilities you require.

Property utilities and connectivity

List the utilities and services you need for your commercial property to operate efficiently. This can include:

- adequate power supply and type (for example, three-phase electricity)

- heating and cooling systems to maintain comfortable working conditions

- sufficient power points for computers and equipment

- suitable water supply and drainage

- broadband speed and reliability, including fibre availability

Older buildings may need rewiring, upgraded heating or air conditioning, or additional toilet and kitchen facilities, so factor potential upgrade costs into your planning.

Planning permission and use

Check whether you may need planning permission or a change of use to run your type of business from the premises. Understanding this early can help you avoid delays or unexpected costs once you have chosen your commercial premises.

Access and parking

Think about how people and goods will reach your business property. Consider:

- proximity to main roads and public transport

- ease of access for deliveries and collections

- accessibility for customers, including disabled customers

- on-site or nearby car parking for staff, customers and visitors

- any need for cycle parking or other sustainable transport options

Option to extend or make alterations

Assess how flexible the commercial real estate is if your requirements change. Look at whether you can make internal alterations, install partitions, expand into neighbouring space, or extend the building in future, subject to any necessary consents.

Long-term business plans

Review your business plan and consider how the business premises you choose will support your long-term direction. Think about potential growth, new services or products, changes in staffing levels, or future technology needs, and whether the property can adapt to these.

Property location

Location is a crucial factor when choosing commercial property. You need to think about where your property should be to suit your customers, workforce and suppliers, as well as your brand image and operational needs. For detailed location factors you should consider, see choose the right location for your business premises. See, choose the right location for your business premises.

Property costs

Your choice of commercial property will also depend on your budget. Whether you rent or buy business premises, likely costs can include:

- initial purchase costs (if buying property), including legal costs and surveyor's fees

- initial alterations, fitting out and decoration

- any alterations required to meet building, health, safety and fire regulations

- ongoing rent (if leasing premises), service and utility charges, including water, electricity and gas

- business rates

- continuing maintenance and repairs

- building and contents insurance

It can be useful to compare the costs of buying business property with the costs of buying business property so you can decide which option is more suitable for your cash flow and growth plans.

Energy performance of the property

Energy efficiency affects both your running costs and environmental impact. Sellers and landlords must provide prospective buyers or tenants with an Energy Performance Certificate (EPC). An EPC shows how energy efficient a building and its services are and provides a good indication of likely energy costs. You may wish to prioritise commercial property for small businesses that offer better energy performance to help control long-term overheads. See Energy Performance Certificates for business properties.

Prioritising your requirements

If your property requirements are too specific, your choice of commercial premises for business may become very limited or too expensive. Divide your property spec into:

- essential requirements that you cannot compromise on

- desirable features that are beneficial but negotiable

This helps you stay flexible and make a balanced decision when comparing different commercial property options.

Considering working from home

Once you have drawn up your list of property requirements, you may decide that working from home suits your needs better, either full-time or as part of a hybrid model. If so, remember that there are important legal, tax and practical issues to consider, including planning, insurance and health and safety. See use your home as a workplace.

Also on this siteMore Case StudiesContent category

Source URL

/content/business-property-specification

Links

Choose the right location for your business premises

How to identify the advantages and disadvantages when choosing a suitable location for your commercial property.

Choosing the right location for your commercial property is a vital decision for any business. Your business premises should be convenient for customers, employees and suppliers, while still being affordable and aligned with your long term plans. When choosing commercial property, you should weigh up the advantages and disadvantages of different locations before committing to any business property.

What location factors should I consider when looking for business property?

To judge the best location for your commercial premises for business, consider the key factors below and how important each one is to your business priorities. These points apply whether you are looking for business premises to rent, business premises to buy, or specific commercial property for a small business.

Footfall

For many businesses – especially in the retail, hospitality or personal services sectors – the level of passing trade can have a major impact on sales and visibility. Busy high streets, shopping centres, or transport hubs can provide higher footfall but usually come with higher commercial real estate costs and business rates.

Competitors in the area

The number and type of competitors nearby can significantly affect your performance. Some businesses, such as estate agents or restaurants, can benefit from clustering together, as customers often compare options in one area. For many other firms, too many direct competitors close by can reduce your market share and profitability, so it is worth surveying the local area carefully before choosing your business property.

Transport links and parking

Good public transport links and local parking facilities make it easier for employees, customers and suppliers to reach your commercial property. Check proximity to bus routes, train stations, cycle paths and major roads, and consider whether there is sufficient, affordable parking nearby for staff and visitors.

Delivery restrictions

If your business relies on regular deliveries or collections, it is important that your commercial premises for business are easy for vehicles to access. Investigate any delivery time restrictions, loading bay rules, or weight limits that could affect your suppliers or logistics operations.

Planning restrictions

Before you commit to a location, make sure the premises can legally be used for your type of business. Check planning permission and local zoning or use classes to ensure your activity is permitted, and identify any restrictions that might limit how you operate or expand in future.

Business rates

Business rates can be a major ongoing cost and vary depending on property value and location. High-profile city or town centre locations can attract higher rates, which may reduce the attractiveness of otherwise ideal business premises to rent or buy. It is important to get an indication of what you may have to pay so you can factor it into your overall budget. See estimate your rate bill.

Local amenities

Local amenities can make a location more attractive for both employees and customers. Staff often prefer working in areas with nearby shops, cafés, childcare, gyms and other services. You may also need convenient access to banking facilities, postal depots and professional services to support day-to-day operations in your commercial property.

Type and image of an area

The nature and reputation of the area can affect how your business is perceived. A location associated with high crime or anti-social behaviour may deter customers and staff, while a well-regarded business district or regeneration area can enhance your image. Think about how the area aligns with your brand and the clients you want to attract when choosing commercial property.

Deciding on your property location

Every location will have both advantages and disadvantages, so finding the right business property is often a balancing act. For example, an office in a rural setting may be quieter and cheaper, but harder for staff, customers or suppliers to access. A prime city centre site may be excellent for visibility and transport links, but more expensive in terms of property costs, business rates and parking.

Location has a major impact on your overall business costs and on the value you get from your commercial real estate. If you need premises in a prime area – for example, to access key clients or benefit from strong footfall – the extra cost may be justified. The key is to prioritise the factors that matter most to your strategy and choose commercial property that offers the best overall fit for your business.

Also on this siteMore Case StudiesContent category

Source URL

/content/choose-right-location-your-business-premises

Links

Legal considerations when choosing business property

What legal obligations and restrictions to consider when choosing commercial premises.

When choosing commercial property, it is essential to understand the legal obligations and restrictions that apply to your business property. These rules affect both owners and occupiers and will influence the suitability of any commercial premises for business, whether you are looking for business premises to rent or business premises to buy.

Planning permission and permitted use

Your commercial property must have the correct planning permission or use class for your type of business. If you intend to change how the property is used, extend it, or alter its layout, you may need to apply for new planning consent or building control approval.

Failing to comply with planning requirements can lead to enforcement action, so always check permitted use before committing to any commercial property for a small business or larger operation.

Building, fire and health and safety compliance

All commercial property must meet relevant building regulations and fire safety standards. You will need to carry out suitable fire risk assessments, maintain fire detection and alarm systems where required, and ensure that escape routes, emergency lighting and fire-fighting equipment are appropriate for your business premises.

You must also comply with health and safety law to protect employees, contractors and visitors, including providing safe access, adequate ventilation, lighting, welfare facilities and a generally safe working environment. See fire safety and risk assessment.

Business rates, stamp duty and other charges

Most business premises to rent or buy will attract business rates, based on the property’s rateable value and local rules. In many cases, stamp duty land tax (or the relevant property tax) is payable on commercial property purchases and some leases, so factor this into your budget alongside rent or mortgage payments.

Clarify in advance whether the landlord or tenant is responsible for business rates, service charges and other recurring costs before you sign any agreement for commercial premises for business.

Landlord, tenant and lease obligations

If you occupy business premises to rent, the terms of your lease or licence will set out your rights and responsibilities. These may cover rent reviews, repairing obligations, service charges, use restrictions, alterations, subletting, break clauses and how and when the lease can be ended.